What Are Bonds and How Do They Work?

This is for the nerds, for sure! Much of what I’m going to teach about bonds is definitional, and at the end, I’ll try to make it practical for you.

What is a Bond?

A bond is a debt owed by an entity to a party that loans money in exchange for periodic payments and an eventual return of the initial amount invested. Think of it like an IOU. Bonds provide a steady stream of income from the issuer of the bond to the bond holder. Bonds are thought to be more reliably income-producing than owning stocks.

Where Can I Get a Bond?

When bonds first come to market, they are offered by the issuer directly to an investor, many times through auctions. However, most of us buy bonds after that initial offering in a secondary market of bond buyers and sellers or through mutual funds that hold a basket of bonds. The most common original issuers are the federal government, state and local governments, and corporations. As a consumer, you can buy bonds through a broker in a similar way that you buy stocks.

Features of Bonds

Bonds have the following common features that determine their value. I will keep the list to foundational components for bond class 101, but there’s a lot more to it.

Face amount: This is the stated value of the bond in dollars, often $1,000, but it can be in other denominations. The face amount is part of how you determine how much income you will receive from the bond.

Coupon: Bonds express the interest rate they pay by the coupon amount. For example, a bond that has a 5% coupon will pay $50 a year on a $1,000 face-value bond.

Payment Frequency: This is the interval at which you will receive the interest income generated by the bond. Semi-annual is common. In that case, you receive two $25 payments six months apart each year. Some bonds don’t pay along the way; you only receive a lump sum at maturity.

Maturity: This attribute dictates how long a bond will pay interest income before an investor gets a return on their original investment. To illustrate this, if I buy a bond for $1,000 and it pays 5% for 5 years, I will receive $50 per year during the five-year term and a return of my $1,000 investment at the end of five years.

Cost: We almost always buy bonds at a value either greater than or less than the face amount. This is because we are buying them from someone other than the initial issuer, and the variable that affects the value of the bond, most prominently the current level of interest rates, could be higher or lower than in comparison to the bond’s coupon. More on that in a minute.

Types, Risks, and Taxes

Below, I’ll explain four types of bonds, including their risk and some unique features of how they are taxed. Each type has various associated risks: default (The risk that the issuer can’t pay you back), interest rate (More on that when I talk about measuring bond returns below), inflation (The risk that your bond income won’t buy as much in the future), and reinvestment (The risk that the income you receive from the bond will earn less in a new investment). All bonds have all of these risks except for one.

Treasury Bonds: These are issued by the US government and are the only type of bond that has no default risk. That’s because it’s backed by the full faith and credit of the United States. You pay federal income tax on the income received, but if you have a state income tax, treasury income is exempt!

Municipal: State and local governments issue these bonds to fund the government and complete projects like building and improving schools. The taxation of these is the reverse of treasury bonds. You pay NO federal income tax on these bonds, but you may owe state tax, depending on who issued the bond and where you live.

Corporate: Companies of various shapes and sizes issue these to raise funds to expand their business. They have no special tax treatment, so all income is taxed like any other ordinary income you receive. Depending on the financial health of the company, the risk of default may be greater or less than that of other companies. Companies are rated for risk, and those with less-than-stellar ratings offer a higher coupon rate to account for their increased risk. The riskiest corporates are called junk bonds, but there are tons of companies (think Apple) that are a low default risk and highly rated.

Zero-coupon: These are always sold at a discount (For example, $500 for $1,000 face value) and have no periodic payments. At maturity, you collect the face value instead of the lower price you paid to obtain the bond, the difference of which represents your returns. You get hit by a phantom tax with these because you have to pay income tax on part of the increased value every year, but you don’t actualize any income to the very end.

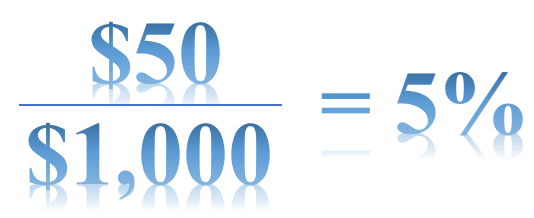

Measuring Bond Returns

Yield measures what income a bond returns to the investor. We can calculate several different forms of yield. At the most basic level, nominal yield is equal to the bond’s coupon. Continuing with our example from above, that is calculated as:

However, another measure of yield, the current yield, can be either higher or lower than the nominal yield. And this concept is where understanding bonds gets a little crazy and tough to keep straight. If this is a bit too much, skip to the end of this article for the practical part.

When interest rates rise, the price of existing bonds goes down. That’s because newly issued bonds in a rising rate environment have a higher coupon than existing bonds, so investors want to sell their 5% bond so they can have a bond that pays 6% instead. You have fewer buyers because who wants $50 a year when you could have $60 from a new 6% coupon bond? When you have more sellers than buyers, the sellers have to accept less than the face amount of the bond if they want to offload it, so someone buying the bond is able to get it at a discount for, say, $909.09. Buying at that lower price causes the bond to have a HIGHER current yield. You get more for your money.

Conversely, when interest rates fall, the price of existing bonds goes up. That’s because newly issued bonds in a falling rate environment have a lower coupon than existing bonds, so investors want to hold onto their 5% bond rather than switch, let’s say, to a 4% bond. You have more buyers because who doesn’t want an older $50 a year bond when you can only get $40 per year from a new 4% coupon bond? When you have more buyers than sellers, the buyers are willing to pay more than the face amount of the bond to have a higher annual income, so someone buying the bond has to pay a premium of, say, $1,111.11 for the privilege of earning $50 per year. Buying at that higher price causes the bond to have a LOWER current yield. You get less for your money.

That understanding has helped me follow bond performance. Have you ever noticed the tickers on Bloomberg or other finance shows? You intuitively understand that higher stock prices are always green because rising stock prices are good. Red stock prices mean the price is falling and indicates you are losing money on your investment. Red means bad, and green means good, right? Yep. So, why is it that HIGHER yield is RED and the LOWER yield is GREEN in the above graphics? When the yield is up (RED), the bond is less valuable ($909 < $1,000); while when the yield is down (GREEN), it’s more valuable ($1,111 > $1,000). The price of bonds and their yield have an inverse relationship. This describes the nature of interest rate risk in bonds.

What Bond Do I Need?

Some of our clients are looking for another steady income stream, while others have a specific goal, like funding college. Depending on your purpose, we select the bonds that fit the profile. If you need income now for living, we may select bonds that return a steady stream for the next 30 years. If you’re in a high tax bracket and want to avoid paying more taxes, municipal bonds could fit the bill. A lot of times, our recommendation depends on the time horizon of your funding goal. We might choose bonds that mature in successive years, starting with your son’s freshman year and carrying him through four years of college. You may need to avoid bonds to reach your goal. If the assets you are investing are for long-term goals (5 years or more), acquiring stock (often through mutual funds or ETFs) achieves a much higher growth rate than bonds. We’ll construct a portfolio that meets your needs, diversifies your risks, and achieves your goals. Book a call to discuss whether bonds make sense for your situation. Once we understand your personal and financial situation and gauge your current investments, we’ll map out a plan to get you where you want to go.

No client or potential client should assume that any information presented or made available on or through this article should be construed as personalized financial planning or investment advice. Personalized financial planning and investment advice can only be rendered after engagement of the firm for services, execution of the required documentation, and receipt of required disclosures. Please contact the firm for further information. The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. Additional information about The Dala Group, LLC is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary report, which are accessible online via the SEC’s Investment Adviser Public Disclosure (IAPD) database at https://adviserinfo.sec.gov/firm/summary/291828